Volatility

How we model volatility in the most volatile energy market in the world.

Why is volatility important?

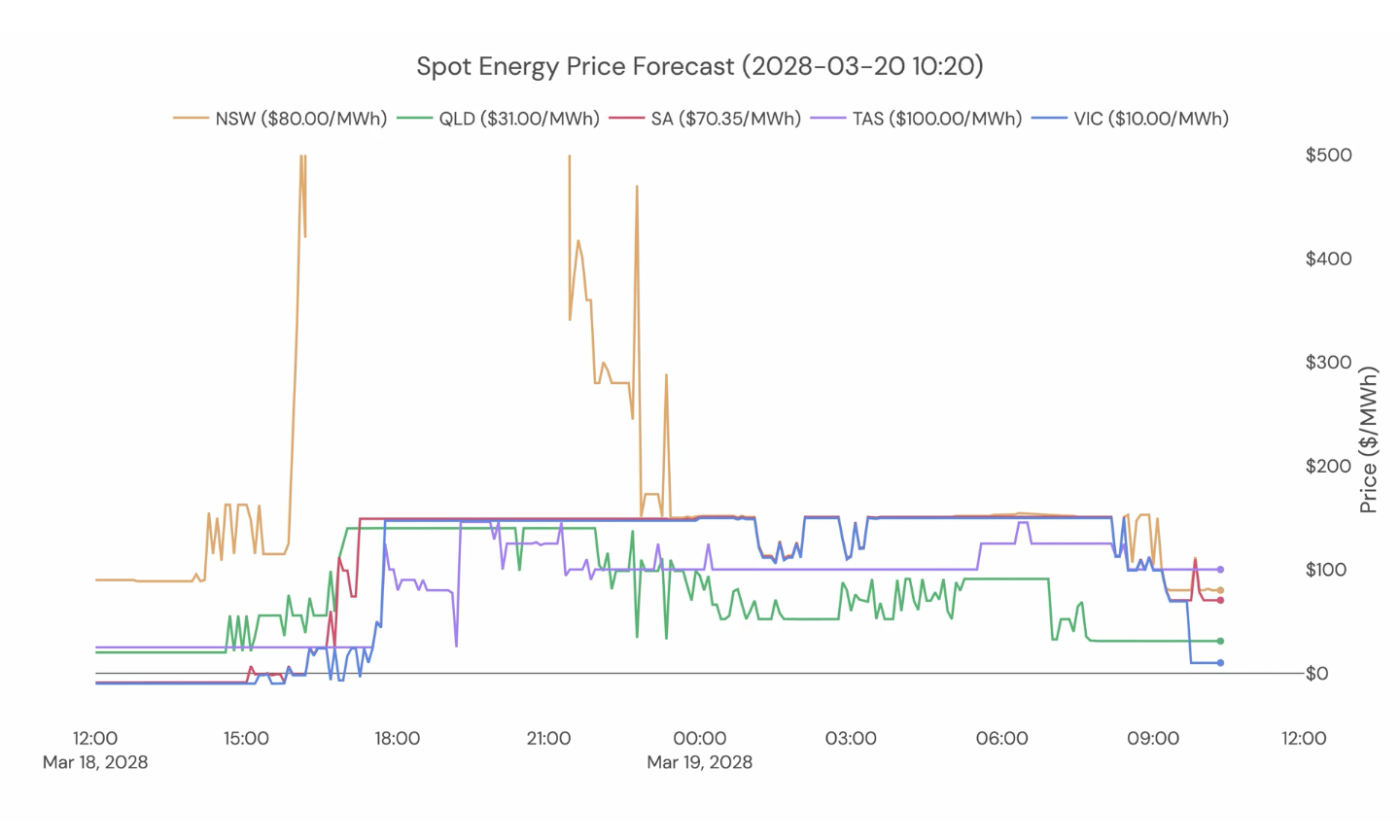

The NEM is one of the most volatile electricity markets in the world. This is due to several factors, but can largely be attributed to a combination of market fundamentals and market design. Market fundamentals that impact volatility include a fleet of ageing coal plants that experience frequent outages, and a stringy transmission grid that can often be heavily constrained. Market design aspects include 5 minute settlement periods, a high price cap, and the lack of a capacity market. This means that peaking assets have to make the majority of their money in the energy spot market through very high bids. The most volatile periods are usually caused by outages of large coal plants or key transmission lines, in combination with periods of high demand and/or low wind and solar generation.

All of this volatility currently produces a significant number of price spikes that can provide batteries with 40% of their revenues. This is one of the most important parts of a battery business case in the NEM and is therefore incredibly important to model properly.

How we model volatility

With volatility being such a fundamental part of the battery business case, it is a huge simplification to simply add in volatility as post-processing. It needs to be a core part of the model.

We model volatility organically by simulating the exact conditions that led to or will lead to volatility. This means forecasting at 5-minute granularity; factoring in generation and transmission outages as well as the impact they will have; properly modelling ramp rates, ramp costs, and start costs; and properly modelling the bidding behaviour of generators - particularly peaking assets such as OCGTs. This is covered in more detail in Thermal generation. We don't decide how much volatility to add in and when to add it. Volatility occurs when the system conditions lead to a tight system margin, either for a specific sub-region, or for a larger part of the NEM. A combination of this and the bidding behaviour of peakers causes price spikes to occur with exactly the same mechanism as lower prices.

Every single year contains volatility, so there is no reason to discount it if it is modelled well. In order to build trust with banks in this volatility value, we thought very carefully about our approach to weather years. We use a weather / outage year that is slightly more conservative than average in order to give full confidence in the level of volatility that occurs in our model.

Capturing all of these dynamics at 5-minute granularity is incredibly complex, and has required extensive backtesting to get right. See our backtest section for more details on how this was done.

Updated 12 months ago